As you know, financial statements can be official and managerial.

Official reporting is submitted by each company in accordance with the requirements of the law. Most often, official reporting includes a balance sheet and a profit and loss statement; these are the information available for most companies.

Rarely - in addition to these documents - official reporting may include:

- cash flow statement,

- statement of changes in equity,

- information about creditors and debtors.

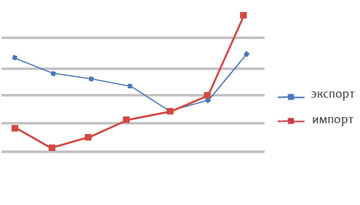

Based on them, you can evaluate:

- scale of the company's activities,

- profitability level,

- the amount of investment in fixed assets,

- structure of own capital and reserves;

- cash flows of the enterprise in current, investment and financial activities,

- the dynamics of these and other indicators.

For the efficient operation of the company, its top management uses management reporting.

The composition of management reporting is determined by industry specifics and the decision-making procedures used by company executives.

Management reporting details the progress and results of various business processes, is prepared with the necessary frequency and detail.

Sometimes part of management reporting is public information, and it may be contained in the company's annual reports or in the issuer's reports, but most of the management reporting is a trade secret of the company, and it is difficult to obtain it.